FACTSHEET: CLIMATE-RELATED FINANCIAL DISCLOSURES

What are Climate-Related Financial Disclosures?

Certain entities will have to make annual disclosures about their climate impact, and what climate change might mean for their business in future, most likely for financial years ending on or after 31 March 2023.

The Financial Sector (Climate-related Disclosures and Other Matters) Amendment Bill (Bill) has been introduced to Parliament which will amend the Financial Markets Conduct Act 2003 to make Climate-Related Financial Disclosures mandatory for certain entities. The Bill has passed its first reading and has been referred to the Economic Development, Science and Innovation Committee. The Select Committee’s report is due on 16 August 2021.

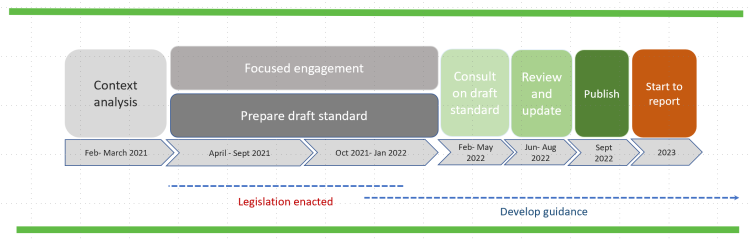

The precise requirements for reporting will be specified in a Financial Reporting Standard to be issued by the External Reporting Board (known as XRB). The XRB intends to consult on the Standard from February to May 2022, publish the Standard in September 2022, and the first Climate-Related Financial Disclosures will be made in 2023. It is expected the Standard will be based on the international Task-Force on Climate-Related Financial Disclosures (TCFD) recommendations.

Climate-Related Financial Disclosures include:

Governance – Describing how the Board and Management deal with climate risks and opportunities.

Strategy – Describing short, medium and long-term climate risks (based on different scenarios – e.g. 1.5C, 2C, 3C) and how they impact the organisation’s financial planning

Risk management – describing processes for identifying, assessing and managing climate risks

Metrics and targets – Disclosing climate risk metrics and emissions targets, and disclosing the methods for measuring performance against those targets.

What type of entities must make Climate-Related Financial Disclosures?

Around 200 large entities will be required to make Climate-Related Financial Disclosures under the Bill. These are:

all registered banks, credit unions, and building societies with total assets of more than $1 billion;

all managers of registered investment schemes with total assets under management greater than $1 billion;

all licensed insurers with total assets under management greater than $1 billion, or annual premium income greater than $250 million; and

all equity and debt issuers listed on the NZX.

Crown financial institutions with total assets under management greater than $1 billion, such as ACC and the NZ Super Fund, have received a letter of expectations from the Minister of Finance in March 2021. But those entities are not referred to in the Bill.

How do Climate-Related Financial Disclosures help NZ’s climate response?

Businesses will be encouraged to implement climate-friendly business practices.

Stakeholders, such as suppliers, customers, and employees, will be able to make informed decisions that align with their values or risk appetite on climate-related issues.

Investors will be able to choose investment schemes or NZX-investments with low climate impact, and they will be able to easily understand the impact of climate change on the future performance of the investment.

Consistency in reporting standards will allow easy comparison between businesses (both in NZ and globally).

When will the regime be implemented?

The XRB’s timeline for developing and implementing the standard for Climate-Related Financial Disclosures is to have consultation on the Standards from February to May 2022 with key stakeholders, with publication of the Standards in September 2022, and the first Climate-Related Financial Disclosures will be made in 2023.

Is the proposed NZ regime good enough?

The proposed regime is a good start. But it the proposed coverage is too narrow. It seems overly focussed on the interests of investors, to the exclusion of other stakeholders such as employees, customers, suppliers – not to mention inhabitants of the planet!

In addition, the narrow coverage is potentially distortionary. We think the crown financial institutions should be subject to the Bill, not just to a letter of Ministerial expectation. In addition, we think government departments, and crown and local authority owned businesses, and large privately-owned businesses or those owned by multinationals, should be subject to the obligations in the Bill, not least because some of them are major emitters and/or compete with listed entities

We fail to see the logic in that unlisted entities (including those owned by multinationals, or by central or local government) not being required to comply, even though their listed competitors will. For example, Ports of Auckland v Port of Tauranga, Mobil NZ v Z Energy, Synlait v Open Country Dairy.

LCANZI’s view is that the regime should be compulsory for a wider range of entities, including privately held companies, trusts, limited partnerships, and central and local government organisations, but with a transitional exemption (for say 5 years) for entities with less than $20m assets/$10m revenue. The transitional exemption for smaller business would be a recognition that it will take time to build the expertise required to report Climate-Related Financial Disclosures.

We will be advocating for these improvements in our submission to Parliament on the Bill.

If your business isn’t required to make Climate-Related Financial Disclosures, should it disclose these risks anyway?

Yes, if you can, you should. We acknowledge that it may take some time and resources to do this.

At some point, all businesses are going to have to grapple with their climate impact, and how climate change will impact them. If your business is proactive about this, you will be better prepared. So why not show it on your website for consumers and investors to see? It is a great marketing tool to show that you are going above and beyond to do your bit to combat climate change.

Given the current state of knowledge about climate change risks, our view is that all directors have an obligation (even without compulsory requirements) to at least consider whether climate risks are potentially material to their company, and to take steps to manage such risks. The proposed Climate‑Related Financial Disclosures framework will present a good way to understand the risks and demonstrate the steps being taken to address them. Some directors are currently doing this, and we encourage all others to do so.